Disclaimer

The information provided in this article is for educational and informational purposes only and does not constitute professional financial, legal, or tax advice. While we strive to ensure the accuracy of the strategies discussed, South African tax laws and investment regulations are subject to change. Every individual’s financial situation is unique; therefore, you should consult with a certified financial planner or a registered tax professional before making any investment decisions. Your Growth Compass is not a financial services provider (FSP), and some links included may be affiliate links that support our platform at no additional cost to you.

You are likely looking for a way to break the cycle of "paycheck to paycheck" living. You want to understand the fundamental difference in how money is managed at different economic levels. You expect to find actionable strategies to stop accumulating "bad debt," identify high-yield assets, and learn how to leverage financial tools specifically available in the South African market to create long-term generational wealth.

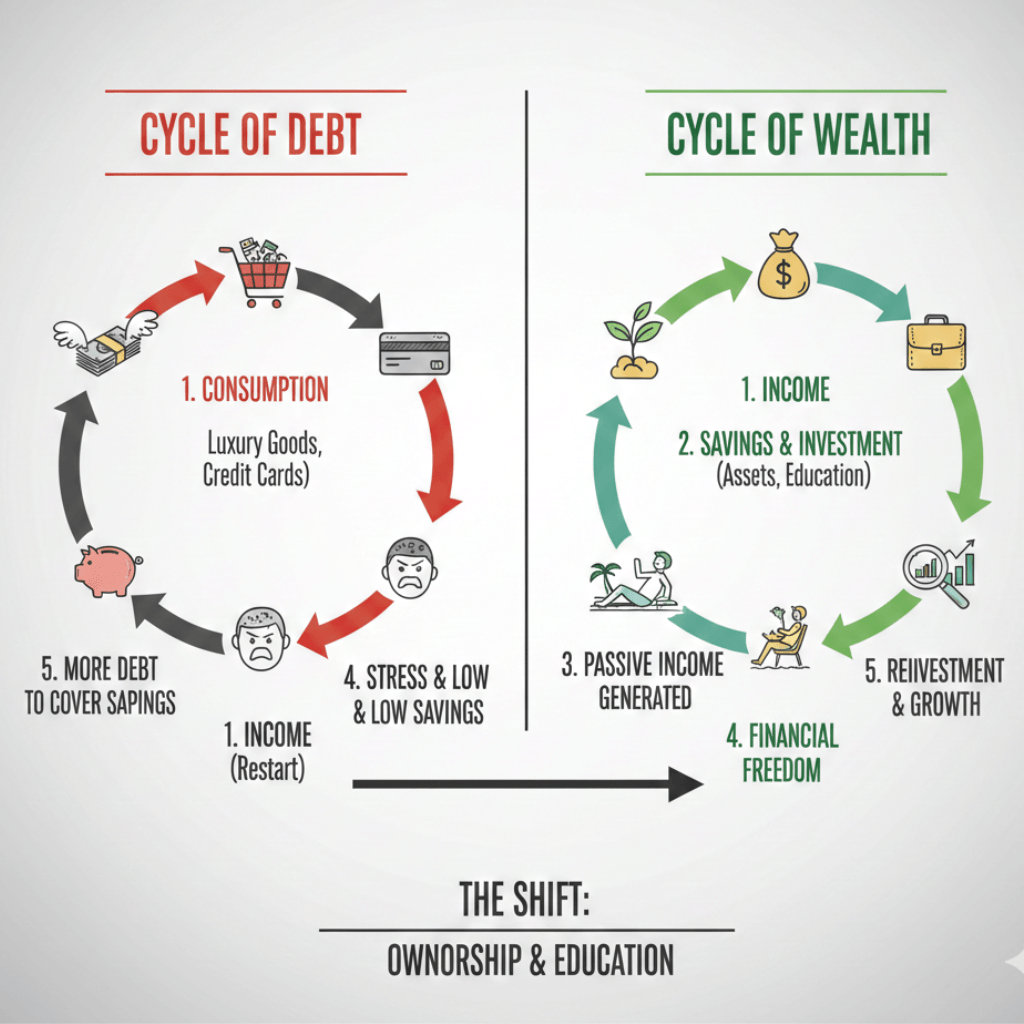

Financial success is rarely about how much money you make; it is about how much money you keep and how that money works for you. In South Africa’s current economic climate, the gap between the rich and the poor is often defined by a single habit: the wealthy build assets while poor people build debt.

While one group spends their income on items that depreciate in value, the other funnels their resources into vehicles that generate more income. If you want to change your financial destiny, you must first change your financial strategy.

Understanding the Core Difference: Assets vs. Liabilities

To understand why the wealthy build assets while poor people build debt, we must define these terms simply. An asset is something that puts money into your pocket. A liability is something that takes money out of your pocket.

Poor and middle-class individuals often mistake liabilities for assets. A flashy car or a high-end smartphone bought on credit may look like wealth, but they are actually "wealth-killers" that drain your monthly cash flow through interest.

1. The Wealthy Prioritize Cash-Flowing Assets

The wealthy focus on acquiring things that provide a recurring return. This might include rental properties in Johannesburg, dividend-paying stocks on the JSE, or a side business. Because the wealthy build assets while poor people build debt, they create a "money machine" that eventually covers their living expenses without them having to trade their time for a salary.

2. How the Rich Use Debt to Get Richer (Good Debt vs. Bad Debt)

Debt is a double-edged sword. Most people use debt to buy "stuff", clothes, vacations, and furniture. This is bad debt because the interest rates are high and the items lose value.

However, if you ask how do the rich use debt to get richer, the answer is leverage. They borrow money at a low interest rate to invest in an asset that yields a higher return. For example, using a bank loan to buy a commercial property where the rent covers the bond and leaves a profit.

Leveraging Other People’s Money (OPM)

By using the bank’s money to acquire assets, the wealthy grow their net worth much faster than someone saving their pennies. They don't fear debt; they respect it and use it as a tool for expansion.

3. Investing in Productive Knowledge and Skills

One of the most overlooked ways to increase your wealth is investing in yourself. While those struggling might spend their free time on cheap entertainment, the wealthy spend it on high-level seminars, books, and coaching. They know that their earning potential is capped only by their level of skill.

4. The Role of Ownership: Equity Over Salaries

A salary is a temporary solution to a permanent problem. The wealthy understand that true freedom comes from equity. Whether it’s owning shares in a global company or a stake in a local South African startup, ownership allows for exponential growth that a fixed hourly wage can never match.

5. Tax Efficiency and Legal Structures in South Africa

In South Africa, the way you own an asset matters as much as the asset itself. The wealthy build assets while poor people build debt often by using legal entities like companies and trusts to protect their wealth and minimize tax.

Why the Wealthy Build Assets While Poor People Build Debt Using Trusts

A trust can help manage estate taxes and protect assets from creditors. While the average person pays tax on their gross income first, a business owner can often deduct expenses before paying tax, leaving more capital to reinvest into new assets.

6. Automation: Building Systems That Work 24/7

Wealthy individuals don't just work hard; they build systems. This could be a digital product, an automated trading portfolio, or a business with a management layer. This systemic approach is a primary reason the wealthy build assets while poor people build debt; they aren't limited by the number of hours they can physically work.

LEARN HOW TO: The Master Blueprint - The FREE 4-Part "Foundation Series" for Systeme.io

7. Delayed Gratification: The "Buy it Later" Rule

The "Poor" mindset seeks immediate comfort. The "Wealthy" mindset seeks long-term freedom. A wealthy person will wait to buy a luxury SUV until their assets, not their salary, can pay for it. By delaying gratification, they ensure their capital stays invested for longer, benefiting from compound interest.

8. Diversification Across Multiple Income Streams

Relying on a single job is the most dangerous financial position to be in. The wealthy seek out various assets that make you rich, such as:

Real Estate (Residential or Commercial)

Equities and Index Funds

Private Equity/Business Ownership

Intellectual Property (Books, Patents, Courses)

Assets That Make You Rich Beyond the Stock Market

Don't ignore alternative investments. In South Africa, section 12J companies (though phased out, similar venture capital structures exist) and physical commodities like gold or silver act as hedges against inflation and currency volatility.

9. Understanding the Time-Value of Money

A Rand today is worth more than a Rand tomorrow. The wealthy move quickly to invest their surplus cash because they understand that every day money sits in a low-interest savings account, it is losing purchasing power to inflation.

10. Building a Network of Wealth-Minded Individuals

You are the average of the five people you spend the most time with. The wealthy surround themselves with mentors and partners who challenge them to think bigger. While others might bond over shared complaints about the economy, the wealthy bond over shared opportunities.

How to Build Wealth When in Debt: A Practical Roadmap

If you are currently struggling, don't lose heart. You can learn how to build wealth when in debt by following these steps:

Stop the Bleeding: Cut all unnecessary credit spending immediately.

The Snowball Method: Pay off your smallest debts first to build momentum.

Micro-Investing: You don't need thousands to start. Use apps that allow you to buy fractional shares for as little as R10.

Increase Income: Use your current skills to freelance and funnel every cent of that extra income into debt repayment and then assets.

Key Takeaways

Assets put money in your pocket; liabilities take it out.

The wealthy use "good debt" to buy income-generating property or businesses.

Ownership (equity) is the fastest path to long-term wealth.

Financial education is the most valuable asset you can own.

Start small, but start now; consistency beats intensity.

Common Mistakes to Avoid

Lifestyle Inflation: Increasing your spending every time you get a raise.

High-Interest Consumer Debt: Using store cards or credit cards for consumables.

Lack of an Emergency Fund: Being forced to take on debt when an unexpected expense arises.

Waiting for the "Perfect Time": Postponing investing because the market seems "volatile."

Conclusion: Start Building Your Asset Portfolio Today

The fundamental truth remains: the wealthy build assets while poor people build debt. By shifting your focus from consumption to contribution and ownership, you set yourself on a path toward financial independence.

You don’t have to do this alone. To help you navigate your first steps into the world of investing, we have created a comprehensive resource tailored for the South African market.

Ready to stop building debt and start building a legacy?

[Download The ZeroTo Invest Checklist FREE PDF here] and take control of your financial future today!

For more insights on growth, visit Your Growth Compass.

Frequently Asked Questions (FAQ)

Yes. Focus on high-interest debt first while simultaneously building a small emergency fund. Once the "bad debt" is cleared, redirect those payments into cash-flowing assets.

Low-cost Index Funds and Exchange Traded Funds (ETFs) via platforms like EasyEquities are excellent starting points due to low entry barriers.

They ensure the asset’s income significantly exceeds the debt’s interest and capital repayments, maintaining a "safety margin" for market fluctuations.

South Africa offers incentives like Tax-Free Savings Accounts (TFSA) and tax deductions for retirement fund contributions, which accelerate wealth building.

The quickest way is to increase your primary income while keeping your expenses low, then aggressively investing the surplus into appreciating assets.

While we focus on South African growth strategies here at the Compass, We’ve moved all our technical 'how-to' training and system-building frameworks over to our global lab, YourStackBuilder.com. If you're ready to build the infrastructure for your ideas, start with The Master Blueprint workshop there.

General Disclaimer: Your Growth Compass is an educational and informational platform, not a registered financial advisory service. All cryptocurrency and investment information provided is for educational purposes only. Bitcoin and other digital assets are highly volatile and inherently risky. We are not liable for any financial losses, profits, or investment decisions you make. Always conduct your own due diligence or consult a certified financial professional before investing

Latest Articles

© 2025 Your Growth Compass SA All Rights Reserved